Have you ever wondered how much the highest-paid CEO in your state makes for a living? It turns out that climbing to the top of the corporate ladder can mean dramatically different things in different parts of the country. Our new map breaks down the highest-paid CEOs in each state, letting you easily see total compensation figures and the companies they work for.

We took compensation numbers from the AFL-CIO’s Executive Paywatch project and replaced each state on a map with a photo of the highest-paid chief executive, together with their employer’s logo. We then color-coded each photo to indicate how comparatively high or low their income ranks—the darkest shade represents over $121M; the lightest shade up to $40M. This approach gives you a quick snapshot of the geography of executive compensation across the U.S.

These are the ten states topping the list on our chart with the highest paid CEOs ($M) (all figures represent 2017 compensation totals unless otherwise noted):

1. Florida: Hunter Harrison, $151.1M at CSX Corporation

2. New York: Frank J. Bisignano, $102.2M at First Data Corporation

3. California: Peter P. Gassner, $88.1M (as of 2018) at Veeva Systems

4. Ohio: W. Nicholas Howley, $61M at Transdigm Group

5. North Carolina: Douglas Lebda, $59.6M at LendingTree

6. Massachusetts: Douglas Ingram, $56.9M at Sarepta Therapeutics

7. Georgia: Ronald F. Clarke, $52.6M at FleetCor Technologies

8. Colorado: Gregory B. Maffei, $47.8M at Liberty Interactive Corporation

9. Illinois: Dirk Van De Put, $42.4M at Mondelez International

10. Maryland: David M. Zaslav, $42.2M at Discovery Communications

This first and most obvious thing our map demonstrates is the wide disparity in executive compensation at the top of the corporate ladder. Hunter Harrison from Florida’s CSX Corporation pulled in $151.1M, about 50% more than the second-place earner, Frank Bisignano from First Data at $102.2M. At the opposite end of the spectrum, Kevin Riley “only” makes $1.8M at Montana’s First Interstate BancSystem. Think about it this way: Kevin Riley makes more than 38 times the average American salary of $46,641, but Hunter Harrison made more than 83 times as much as Riley! In short, executive compensation skyrockets depending on a number of factors, but the figures definitely tend to reflect the economic status of the U.S. in general, varying widely based on location.

At a macro level, our map highlights the fact that the highest-paid CEOs are clustered in a select few coastal states. CEOs living along the Atlantic Seaboard generally make the most. In fact, there are only two states west of the Mississippi where the top-paid CEO makes over $40M: Gregory Maffei in Colorado ($47.8M) and Peter Gassner in California ($88.1M as of 2016). Also of note, almost all the CEOs on our map are white men, and only a handful are women. This is additional evidence in support of the hotly-debated gender and diversity pay gap within boardrooms in corporate America.

There are a couple of key caveats to keep in mind. Companies pay their executives with more than just simple cash salaries. The numbers behind our map might include vested company stock, unvested stock, other stock options, private security detail, or the use of a private jet—all these things factor into overall CEO compensation. You may have also noticed that high-profile CEOs like Jeff Bezos, Elon Musk, and Warren Buffett are missing from our list. That’s because they own large parts of their companies, so they don’t take a salary the same way these CEOs do.

Want to learn more? A new SEC ruling now requires companies to disclose the average pay gap between CEOs and workers at each company. Check out our other articles detailing companies with the best and worst pay gaps in the country.

We got the data for our visualization over at

We got the data for our visualization over at We got our numbers directly from the

We got our numbers directly from the The

The We pulled our numbers from the

We pulled our numbers from the  We found the numbers for our visualization thanks to the

We found the numbers for our visualization thanks to the We found the data for our visualization from

We found the data for our visualization from Our data come from the

Our data come from the

The data for our visualization come from

The data for our visualization come from We found the numbers for our maps from the

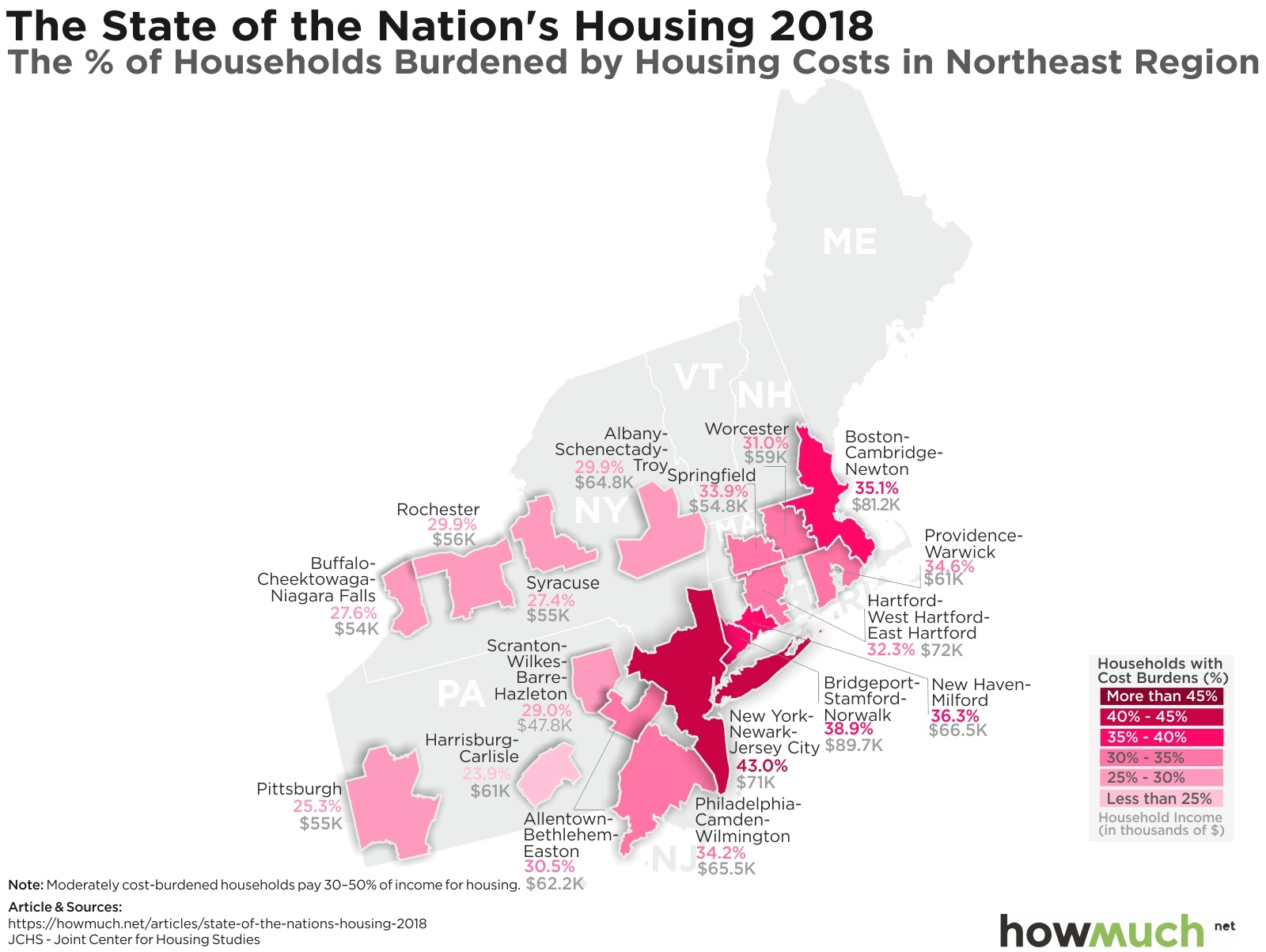

We found the numbers for our maps from the Taking a closer look at the Southwest reveals the extent of the problem. Stretching from San Francisco along the Pacific toward San Diego, between 30-45%+ of the population struggle to pay for housing. San Jose represents a fascinating case study of inequality. The average household income is $109,200, and yet 36.5% of people have trouble paying for their homes. In a word, that’s due to gentrification. People with high-paying jobs in Silicon Valley can afford to pay expensive prices, but that drives up the prices for everybody else too.

Taking a closer look at the Southwest reveals the extent of the problem. Stretching from San Francisco along the Pacific toward San Diego, between 30-45%+ of the population struggle to pay for housing. San Jose represents a fascinating case study of inequality. The average household income is $109,200, and yet 36.5% of people have trouble paying for their homes. In a word, that’s due to gentrification. People with high-paying jobs in Silicon Valley can afford to pay expensive prices, but that drives up the prices for everybody else too. The situation is similar across pockets of the Northeast, in particular in the greater New York and Boston areas. Places like Bridgeport, CT have comparably high average household incomes ($89,700) but shockingly high figures for housing cost burdens (38.9%). Let’s spare a thought for Pittsburgh, though, where the average household makes significantly less at $55,000 and 25.3% of the population struggles to pay for housing. These numbers hint at the pockets of poverty that exist in old manufacturing centers.

The situation is similar across pockets of the Northeast, in particular in the greater New York and Boston areas. Places like Bridgeport, CT have comparably high average household incomes ($89,700) but shockingly high figures for housing cost burdens (38.9%). Let’s spare a thought for Pittsburgh, though, where the average household makes significantly less at $55,000 and 25.3% of the population struggles to pay for housing. These numbers hint at the pockets of poverty that exist in old manufacturing centers. Speaking of the Rustbelt, take a look across the Midwest. Chicago immediately stands out as the place with the highest share of housing burdens at 35.0%, which is several points above every other metro area in the region. The city with the highest average incomes is further north in Minneapolis-St. Paul at $71,700. The relatively low rates of housing burdens combined with reasonable income levels makes us believe the Midwest is the best overall place for housing in the country.

Speaking of the Rustbelt, take a look across the Midwest. Chicago immediately stands out as the place with the highest share of housing burdens at 35.0%, which is several points above every other metro area in the region. The city with the highest average incomes is further north in Minneapolis-St. Paul at $71,700. The relatively low rates of housing burdens combined with reasonable income levels makes us believe the Midwest is the best overall place for housing in the country. Taking a look across the South demonstrates a slightly worse situation than the Midwest. There are clearly several metro areas with significant problems, notably Virginia Beach (35.2%), New Orleans (36.2%), Orlando (37.6%) and Miami (45.7%). But what stands out to us is actually McAllen, TX, along the US-Mexico border. 31.8% of the population struggle to pay for housing on average incomes of only $36,700. These numbers indicate a severe level of poverty combined with a shortage in affordable living spaces.

Taking a look across the South demonstrates a slightly worse situation than the Midwest. There are clearly several metro areas with significant problems, notably Virginia Beach (35.2%), New Orleans (36.2%), Orlando (37.6%) and Miami (45.7%). But what stands out to us is actually McAllen, TX, along the US-Mexico border. 31.8% of the population struggle to pay for housing on average incomes of only $36,700. These numbers indicate a severe level of poverty combined with a shortage in affordable living spaces. We gathered the data for our visualization from

We gathered the data for our visualization from Car insurance can be a little confusing, so let’s break things down. Think about it like this: say you’re driving down the road and run into another car, causing significant damage and injuring the other driver. Liability coverage only protects the people you hit. Collision coverage is different, it would pay for the damage to your own vehicle even though you caused the crash. Comprehensive coverage provides another layer of protection, for example in case the weather damages your car.

Car insurance can be a little confusing, so let’s break things down. Think about it like this: say you’re driving down the road and run into another car, causing significant damage and injuring the other driver. Liability coverage only protects the people you hit. Collision coverage is different, it would pay for the damage to your own vehicle even though you caused the crash. Comprehensive coverage provides another layer of protection, for example in case the weather damages your car. We gathered the information for our visualization from

We gathered the information for our visualization from The numbers for our map and visualization come from Zillow’s housing data for March 2018, but our friends at

The numbers for our map and visualization come from Zillow’s housing data for March 2018, but our friends at We also wanted to visualize the numbers another way to understand the total cost of living across the US. We created a stacked bar chart comparing average monthly mortgage payments (pink) and monthly rent payments (blue). This approach lets you easily see which states have a significantly higher cost of living, and which are relatively cheap in comparison.

We also wanted to visualize the numbers another way to understand the total cost of living across the US. We created a stacked bar chart comparing average monthly mortgage payments (pink) and monthly rent payments (blue). This approach lets you easily see which states have a significantly higher cost of living, and which are relatively cheap in comparison. We found the numbers for our visualization from

We found the numbers for our visualization from  We found the data for our exploding pie chart at

We found the data for our exploding pie chart at We created the data behind our map thanks to the research tools at

We created the data behind our map thanks to the research tools at We gathered the data from the

We gathered the data from the